Drier than a good martini

When testing a document with consumers they got the following feedback:

“Who is the target audience for this? It certainly does not appear to be aimed at me. Drier than a good martini.”

I thought "Yes, I've been there!". In financial services you can be working on documents thinking "I know what this is about, I've written part of it and even I'm bored." Sometimes you spend hours working on a product journey with the gut feeling that no one will read these documents. It's an uncomfortable truth in financial services. One that we should be striding (not edging) away from in the new Consumer Duty world.

Legally you want to protect the parties so you try to cover every risk. Sometimes you'll get stakeholders who'll challenge and say "do we really need this?". You get brave and remove term X, 3 months later you get a string of complaints that your terms and conditions aren't clear enough as there is no mention of X.

Conversely it can actually be financial services regulation that restricts you, especially in the consumer credit sphere. You might have a team of product, risk, marketing, digital, user experience (UX) and user interface (UI) managers all willing to adapt or remove something. Then the lawyers come in and unhelpfully say "this needs to stay or the contract will be unenforceable under the regulations". When you have an Adequate Explanation document (explaining key terms), a Pre Contract Credit Information (PCCI) document with more explanations and prescribed terms and a Credit Agreement with further prescribed terms, you can easily why people switch off! Role on consumer credit reform.

A bit mealy mouthed

At the opposite end of the scale, when you try to distil information down you can actually go too far resulting in pointless communications.

When testing ESG fund communications, The Wisdom Council found that vague words reduced trust. One consumer commented that a communication was:

"a bit mealy mouthed as it 'seeks to adhere to' which basically could mean anything."

Again I thought "I've been in those kind of discussions". There could be a feature of the product that could be explained in a face-to-face chat in 2 minutes. The term in the contract is however 250 words. When it comes to marketing you have a range of assets with different limits. You may try to break this feature down into a bullet point for an ad in an online newspaper. However when it comes to your carousel of social media posts this feature only gets a 100 character limit. If you go beyond that then the content may trigger additional risk warnings.

Firms can get to a place where they think the choice is between:

(a) a simple message that ultimately means nothing; or

(b) a longer message with five caveats that no one will read on a phone screen.

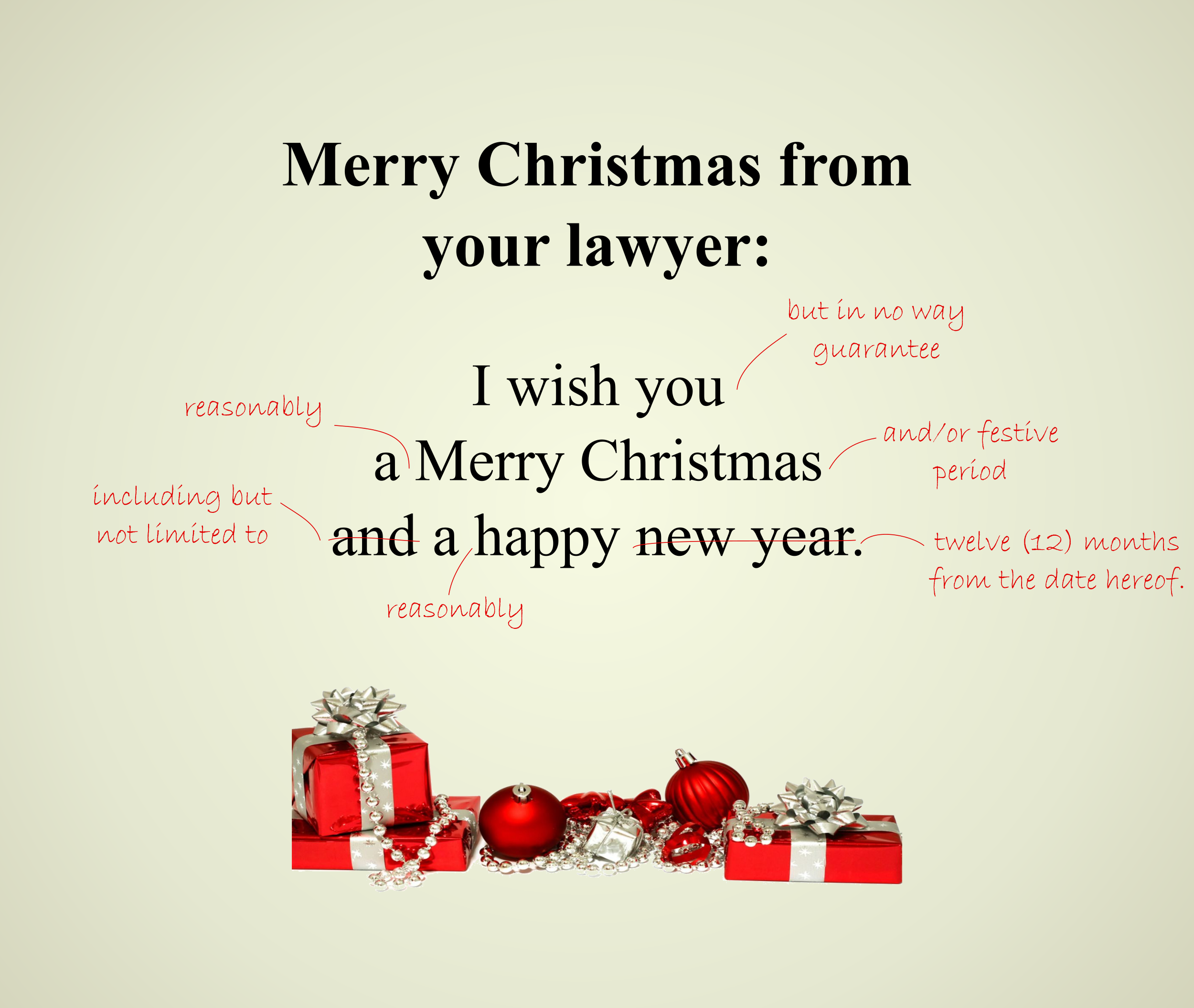

I get it, financial services firms don't want their customer communications looking like the meme of a Christmas card from a lawyer:

Some might argue that lawyers should not be allowed near marketing at all. However the regulated nature of financial services means that legal risk should not be disregarded. A social media influencer may be happy to "collaborate" with a firm but that doesn't mean the influencer understands that they could be committing a criminal offence by promoting a financial services product without FCA authorisation.

Up to now Financial Conduct Authority (FCA) rules on financial promotions have been technology neutral. The rules were written long before anyone thought about the connotations of certain emojis. The FCA recently consulted on guidance on how their financial promotion requirements apply to promotions on social media, GC23/2. After receiving feedback, the FCA intend to publish guidance later in 2023.

Whilst we await the final guidance, we all need to get better at getting the basics right across the board. Rather than just reacting to an asset that lands in an inbox for approval, we need to start with "who is this for?" and "what is the point?". There can be a tendency to keep pushing with something because of the sunk cost. You can be better going back to the original brief.

Firms have been trying to overhaul documents, journeys and communications recently. There has a been a lot of consumer testing with interesting feedback. Whilst the Consumer Duty implementation date has passed the industry doesn't get to relax, this is just the start of a continual effort to make things better. As an industry we need to get to the place between "drier than a good martini" and "a bit mealy mouthed".